Sopheon plc, the InnovationOps software company, is pleased to announce its results for the year ended 31 December 2022, together with an outlook for the current year.

Financial Highlights:

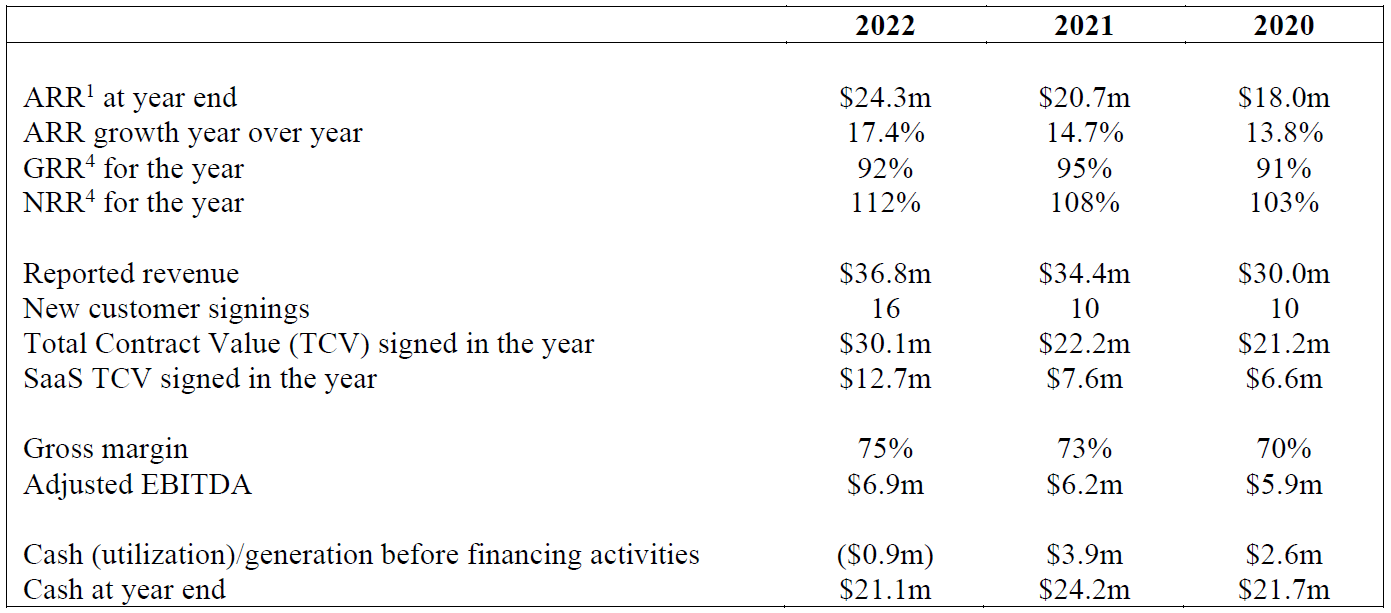

- Revenue of $36.8m (2021: $34.4m) in line with market expectations - and ahead on a constant currency basis

- ARR1 rose to $24.3m at the start of 2023 from $20.7m a year before, growth of 17.4%

- Full year 2023 revenue visibility2 stands at $28.4m (last year at this time: $25.1m)

- Gross ARR retention at 92% (2021: 95%) – Net ARR retention at 112% (2021: 108%)

- Adjusted EBITDA3 of $6.9m (2021: $6.2m) also ahead of market expectations

- Profit before tax $1.3m (2021: $1.2m) after absorbing $2.2m of M&A related amortization and intangible impairments

- Net cash of $21.1m (2021: $24.2m) reflecting currency movements, M&A and other factors. The group has no debt and has always had cash balances spread across multiple global banks.

- Dividend to be maintained at 3.25p per share (2021: 3.25p)

Operational Highlights

- 16 new customer wins (2021: 10) for Accolade, all but one signed as SaaS, underlining our strategic shift to SaaS for all new customers. We also converted 13 existing clients (2021: 6) to SaaS. Concluded the largest order in the company’s history with the US Navy, an existing customer, boosting total contract value signed in the year to over $30m (2021: $22m).

- Integrated two acquisitions – ROI Blueprints, acquired at the end of December 2021, and Solverboard, acquired in May 2022.

- Launched three software-as-a-service (SaaS) products under the Acclaim™ banner: Acclaim Ideas (formerly Solverboard), Acclaim Projects (formerly ROI Blueprints), and Acclaim Products (internally created). The launch of these new solutions expands Sopheon’s addressable market by an estimated $2bn and boosts the Company’s position as the leading software vendor focused on operationalizing the business of innovation.

- Our balance sheet remains very strong to fuel additional acquisition and investment. Our recent appointment of Barney Kent, former chief operating officer of Ideagen plc as a non-executive Director, underlines our commitment to both organic growth and M&A activities.

Outlook

Andy Michuda, Chairman, commented: “Sopheon delivered solid growth with record ARR last year, and acquisitions and new products tripled our multi-billion-dollar addressable market. Our ambition is for Sopheon to double run-rate revenue every three to four years, with world class margin and retention metrics. This will require a contribution from acquisitions, on top of accelerated organic growth. We start 2023 with a strong foundation of ARR, a stable of new products, and a growing sales pipeline. I look ahead with both excitement and confidence, anticipating continued delivery this year alongside rising velocity in our business.”

For further information contact:

| Andy Michuda (Chairman) Arif Karimjee (CFO) |

Sopheon plc | + 44 (0) 1276 919 560 |

| Carl Holmes/ George Dollemore (Corporate Finance) Alice Lane/Sunila de Silva (ECM) |

finnCap Ltd | + 44 (0) 20 7220 0500 |

About Sopheon

Sopheon (LSE: SPE) provides complete Innovation Management software and expertise to help customers achieve exceptional long-term revenue growth and profitability. Sopheon’s Accolade and Acclaim offerings deliver unique, fully integrated coverage for the entire innovation management and product development life cycle. Sopheon’s leadership in innovation management was highlighted in the comprehensive MarketsandMarkets™ report on the Innovation Management Market where Sopheon was listed in the “Stars” category, the highest recognition. Sopheon’s solutions have been implemented by over 200 customers with over 125,000 users in over 50 countries. Sopheon is listed on AIM, operated by the London Stock Exchange. For more information, please visit www.sopheon.com.

1 ARR is the annual value of all ongoing contracts for SaaS, hosting and maintenance in force at the measurement date including pending renewals but excluding confirmed terminations.

2Revenue visibility comprises revenue expected from (i) closed license orders, including those which are contracted but conditional on acceptance decisions scheduled later in the year; (ii) contracted services business delivered or expected to be delivered in the year; and (iii) recurring maintenance, hosting, SaaS and rental streams. The visibility calculation does not include revenues from new sales opportunities expected to close during the remainder of the year.

3Adjusted EBITDA is defined and reconciled in Note 5 to this report

Sopheon, Accolade, and Acclaim are trademarks or registered trademarks of Sopheon plc. All other trademarks are the property of their respective owners.

Chairman’s Statement

The global economy entered tremendous turmoil in 2022 with conflict, inflation and stagnation. In this chaotic environment, all companies face an accelerating and insatiable demand to deliver innovation - the products and experiences that delight customers, drive revenues and loyalty, and secure market share.

In one of the most chaotic business environments I’ve seen in my career, the opportunity for Sopheon has never been greater. Our InnovationOps software reduces the chaos and inefficiencies of innovation operations, harmonizing the discovery, design and delivery of new products and services. Our customers increase the speed, and reduce the risks and costs, of bringing innovative products to market. The very products that expand market opportunities and modernize brands for the future.

Sopheon exited 2022 with two successful acquisitions and grew from a single product company to a family of four products, tripling Sopheon’s addressable market to almost $3 billion. Sopheon’s combined family of InnovationOps solutions offer a compelling and unique value proposition for companies: automate and provide a single source of truth to eliminate the innovation stalls, stumbles and failures that are completely avoidable in even the most chaotic of times.

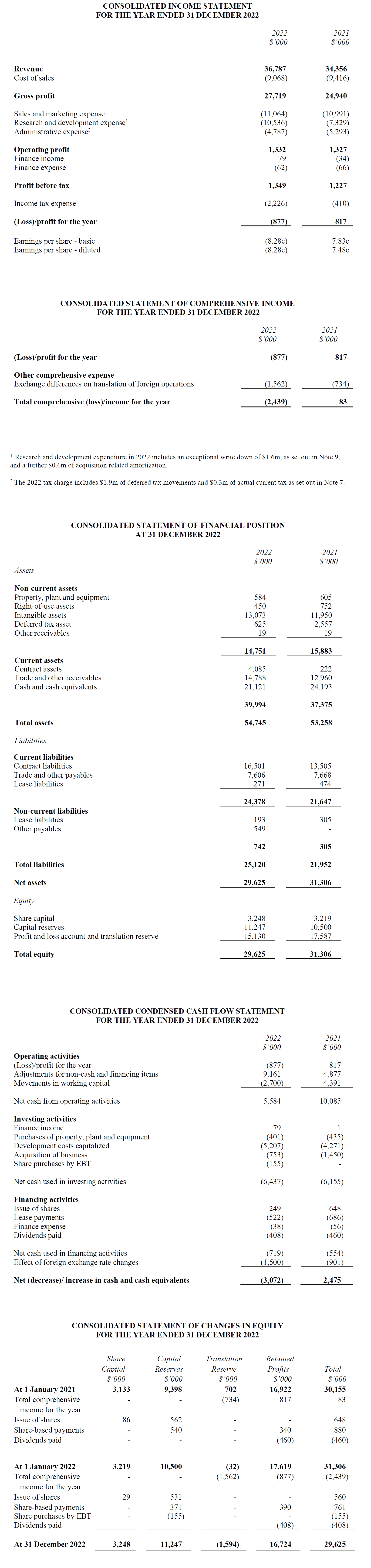

Our financial performance illustrates the initial success of our efforts. ARR increased 17.4% to $24.3m (2022) compared to $20.7m (2021). Top line revenue rose to $36.8m compared to $34.4m in 2021. At constant currency, revenue would have exceeded $38m, representing 10% organic growth. Total contract value (TCV) of all sales closed in the year exceeded $30m up 35% year over year – with the exceptional outperformance attributable to signing the largest single deal in our history with the US Navy. Adjusted EBITDA improved by almost 12%, rising to $6.9m (2022: $6.2m) while taking a $1.6m write down in respect of technology investments superseded by the acquisitions, as well as $0.6m in M&A amortization.

More than 90 percent of our new customers signed SaaS contracts in 2022, and our installed base continues to convert from perpetual to SaaS subscriptions. We intend to sell all new customers on a SaaS basis and continue converting existing customers to this model. Although we expect perpetual license sales to fall in 2023 and 2024, this will be offset by growth in ARR. This will naturally slow revenue and profit development in 2023 but is expected to accelerate more predictable ARR growth in subsequent years. We expect this to come through clearly as we enter 2024, delivering higher growth and profitability from that point forward.

Our ambition is for Sopheon to then double run-rate revenue every three to four years, with world class margin and retention metrics. This will require a contribution from acquisitions, on top of accelerated organic growth, plus constant improvements in structure, policies, processes, and systems. A proactive acquisition strategy will continue to add earnings-enhancing benefits to investors, but also product depth and breadth as Sopheon moves into a phase of controlled and sustainable growth.

We have an incredible team of employees, our SaaS solution revenue continues to grow, and our balance sheet remains very strong to fuel additional acquisition and investment. Our recent appointment of Barney Kent, former COO of Ideagen plc, as a non-executive Director underlines our commitment to both organic growth and M&A activities.

We start 2023 with a strong foundation of ARR, a stable of new products, and a growing sales pipeline. I look ahead with both excitement and confidence, anticipating continued delivery this year alongside rising velocity in our business.

CEO Review: A year of Progress and Resilience

2022 was a year of demonstrated resilience and accomplishment for Sopheon. The company significantly advanced many of the key aspects of its business. Internally, we continued to deliver against our stated plans to expand our products and services, through both acquisition and organically, while significantly progressing to become an enterprise SaaS/cloud company focused on innovation management and product development. The company also responded well to the many external global impacts: the ‘Great Resignation’ in which companies globally felt the impact of increased departure rates in the wake of the COVID-19 pandemic; the Russian-Ukraine War and its effects commercially; customers who experienced major supply-chain chokepoints; climate-exacerbated natural disasters and political upheavals in many countries where we do business; and the significant rise of inflation after 40 years at rest.

Despite these challenges, throughout 2022 Sopheon stayed committed and focused on our strategy and goals. We continued to deliver value to our existing blue-chip customers and added new premium customers globally. Companies continued to invest in innovation products and processes to deliver on their goals of growth, efficiency, productivity, and competitiveness. As a result, Sopheon delivered on both growth and profitability with a significant increase in ARR and Adjusted EBITDA, exceeding expectations. These impressive financial results were achieved alongside major strategic accomplishments. We launched three new products—two derived from acquisitions absorbed in the year, and the third developed organically. This enabled us to expand our end-to-end capability to operationalize innovation, offering immediate value to both corporate executives as well as their supporting cross-functional teams, significantly expanding our addressable market. We call this InnovationOps which is described further below. As a business that has focused on the business of innovation since our start, Sopheon is uniquely positioned to deliver on the promise of InnovationOps.

During the year we continued several key themes that I outlined in our 2021 annual report:

- Growth: We exceeded our goals for both ARR and Adjusted EBITDA growth while achieving 5% revenue growth.

- More: We added to our family of products and services through both acquisition and internal development. Two acquisitions and new internally developed products and services help us deliver more value to current customers and serve new customers and markets.

- Speed: We improved our product development velocity and decreased time to value for new customers.

- Visibility: Increased investment is paying dividends as we are becoming better-known in our primary market and as we expand into new markets with a broadened product set.

- People: We have kept a substantial number of long-standing key contributors while attracting new talent in all areas of the company.

How were we able to achieve these results?

- Focused on SaaS/cloud sales of our flagship product Accolade. Our global sales and services teams targeted existing on-premise customers to move to our cloud offering. Generally, this is mutually beneficial, as most enterprises have preferred cloud hosting and the SaaS model since 2016. This transition to SaaS/cloud increases predictability of revenues, offers better growth potential and delivers greater lifetime value to displace acquisition costs. Ultimately, this is about better quality of revenue overall, and is reflected in our 17.5% increase in ARR. Thirteen existing Accolade customers moved to a SaaS model, and most Accolade customers are now SaaS or cloud hosted. All new products introduced in 2022—Acclaim Ideas, Acclaim Products and Acclaim Projects—are native multi-tenant SaaS offerings.

- Broadened our offerings through acquisition and internal development. Throughout 2022, we filled out our portfolio of products which was critical for us strategically and competitively. Accolade continues to offer unique, differentiated value to customers looking to add needed governance to their innovation processes, manage their strategy/execution processes, and maximize value from their portfolio of products. As we committed to in 2021, we wanted to expand value for our current clients and gain new customers through multiple market offerings. We achieved that in 2022. With the acquisition of ROI Blueprints, now Acclaim Projects, we address a long-standing competitive opportunity that lets us deepen our relationship with existing customers and win more net new business. With Acclaim Ideas, formerly Solverboard, we address another long-standing market need of managing the discovery process at the front end of innovation. This allows us access to more prospects earlier in their innovation journey. Finally, with Acclaim Products we address an enormous complementary market in product management, a role often responsible for innovation initiatives. For the first time, we have an offering for product managers as individuals. The Acclaim product family provides Sopheon a new and differentiated go to market in 2023.

- Introduced new pricing models. Continuing to modernize our business practices, we simplified our pricing to allow easier selection and consumption of our Accolade and Acclaim Projects software, streamlining the buying journey and easing sales processes. We also introduced usage-based pricing, a consumption-based pricing model in which customers are charged to the extent they use a product or service, rather than on an arbitrary number of individual users. Our new models are based on the number of products or projects a customer manages and have proved popular for customers who want to reduce surprises associated with user-based pricing. In addition, for Acclaim Products and Acclaim Ideas product-led software, we display our pricing on our website and allow online purchasing. Today's B2B buyer is habituated to transparency. Most buyers want to understand price as part of their self-discovery journey, and as a result we want to have a frictionless experience for these end-user offerings.

- Strengthened executive leadership. We strengthened our leadership in two key areas: product development and marketing. During 2022 we added Peter Loerincs to head software development and Heather MacIntosh as our Chief Marketing Officer. Peter has held many roles in his successful career: he has been a software consultant, developer, development manager, leader of product management and development, solution architect and business consultant, with much of this experience directly related to the New Product Development (NPD) and Innovation space we serve. And different from many in engineering or development roles, he has been customer-facing, and with some of the most recognized companies globally. Similarly, Heather Macintosh brings to the CMO role at Sopheon a diversity of career experience, including sales, business development, partner marketing, corporate marketing, product management and more. Heather has served in senior leadership roles most of her career, helping various technology organizations with complex offerings successfully scale their businesses.

- Continued customer centricity. As a company, Sopheon values three attributes: entrepreneurial innovation, team empowerment, and customer enthusiasm. In this last pillar of our values, customer service plays a critical role, especially as we continue to move to a SaaS/cloud organization. SaaS customers can switch more easily to competitive offerings, and it is only through customer success that retention and expansion can occur. In 2022, we achieved a Net Promoter Score of 34, which is in the “great” zone and well within industry norms. Sopheon had a Net Retention rate of 112%, indicating growth above the 100% industry median. In addition, we achieved a Gross Retention Rate (GRR)4 of 92% compared to an industry benchmark of 90%. Organizationally, we have moved all our post-sales activities including consulting, services support, and success under one roof with one leader, for a seamless and optimized customer journey.

Sopheon succeeded in 2022 despite the challenges we faced externally and the continued changes we made internally. We did this by being disciplined and staying focused on executing our stated strategy. As the great management consultant Peter Drucker stated, “The best way to predict the future is to create it.” Sopheon continued to create that future in 2022 and has built a foundation for future success as it goes to market in 2023 with new products, new services, experienced leadership, flexible pricing models, and new go-to-market execution.

4Gross Revenue Retention (GRR), which we have reported for many years, is the percentage of ARR retained at the end of the year from the customer base at the start of the year, not counting revenue from new customers, upsells or price increases. Net Revenue Retention (NRR) is the percentage of ARR retained at the end of the year from the customer base at the start of the year, not counting revenue from new customers but including upsells and price increases.

Why is successful innovation elusive?

As the external forces we saw in 2022 continue and market focus returns to profitable growth, innovation and new product development are even more important for long-term competitiveness and financial performance. However, after decades of organizational attention, and with global R&D spending reaching $2.47 trillion in 2022, the following sad truths remain:

- 40-50% of innovation and new product initiatives fail

- 90% of executives are disappointed with their company’s innovation performance

The late Clayton Christensen, who was known for his focus on innovation as a business consultant and academic, wrote in his book, The Innovator’s Solution:

“More than 60 percent of all new product development efforts are scuttled before they ever reach the market. Of the 40 percent that do see the light of day, 40 percent fail to become profitable and are withdrawn from the market.”

This means that 76% of all NPD efforts fail to make it to market or become profitable. Similar findings underscore the same level of risk and failure in innovation. Companies waste a lot of resources and effort for little or no return. This rate of failure should be unacceptable, regardless of the size of the company. With companies facing an economic crisis caused by a global pandemic, any failure rate above 50% is just not acceptable. So, if a company wants to navigate the crisis and emerge stronger, what should they do? How can they minimize their failure rate?

And most importantly, why does this continue to be a real, consistent, and significant problem that must be addressed by businesses that value innovation and its benefits of growth, efficiency and profitability?

In a recent best practice report, the Product Development Management Association (PDMA) points to what makes innovation difficult to solve: “Firms must continually evolve their NPD capabilities just to ‘stay in the game’ as the business and technology environments change. No one single practice is required for greater innovation performance. Rather, the best firms are better at employing and skillfully combining a variety of NPD capabilities and practices.

We agree with PDMA’s point of view and see organizations still struggle with challenges that cause chaos and prevent them from achieving their innovation goals. The following challenges waste trillions of dollars a year in investment and shareholder value:

- Organizational misalignment

- Disconnected efforts

- Strategy not driving execution down to the individual team member

- Ad hoc tools

- Limited governance to responsibly manage business and commercial risk

Adding to the challenge of successful innovation are three current market trends that continue to have a profound effect on companies – digitalization, sustainability and continuous evolution of customer needs. These trends make it even more difficult for companies to reign in the turmoil and get their innovation and product programs on the right track.

Despite the chaos, predictable and repeatable innovation is not an oxymoron. Sopheon has been working with clients of all sizes and across a wide range of industries over the last 20 years to address the turbulence, including helping them to successfully embrace these current market trends.

The road ahead.

Companies are realizing that managing innovation, mandating innovation, or separating innovation into a stand-alone group doesn’t generate the breakthrough to incremental innovations needed for long term growth and profitability. They see that in leading corporations like 3M, Hershey and Honeywell, innovation permeates all parts of the organization. To achieve this, companies must learn what it takes to operationalize innovation, just as they have learned from the success of software development and product management organizations as they operationalize their environments through DevOps and ProductOps. Companies see that those same principles can be applied to Innovation through InnovationOps.

The innovation market defines InnovationOps as:

The combination of cultural philosophies, practices, people, and tools that increase an organization's ability to deliver innovation at scale.

For decades, we have been saying that, to perform innovation at scale, an organization must operationalize innovation by bringing together the following three areas:

- The people—from team members to executives—across the organization

- The tasks that the people perform across the organization

- The processes that people performing tasks use to ensure repeatability and predictability

As a result of Sopheon’s investment over the past several years, we have rolled out a differentiated family of software and services that enables companies to deploy InnovationOps across the organization and enables the synchronized system to deliver innovation at scale. Each offering is focused on specific innovation tasks that, when brought together with the people and processes across the organization, make InnovationOps a reality.

From individual team members to the CEO, we cover the full spectrum of the tasks that product, innovation, and project professionals must accomplish to drive innovation across their companies. And the result?

For any company that values their investment in innovation, Sopheon can provide all the benefits of InnovationOps: a set of products, that together, creates efficiency that in turn gives innovators better visibility to mitigate uncertainty, reduce risk and make better decisions. It's the essence of the benefit Sopheon has delivered for years with Accolade and that is now extended through our new Acclaim offerings.

Financial Review

Sopheon delivered both strategic and financial progress in 2022, in the face of tough global economic conditions as well as the short-term pressure from our own strategy to migrate our business model to a more recurring revenue basis for higher growth and predictability in future. The Board considers ARR as the driver for long term growth and shareholder value, and therefore this is our primary growth metric and focus. Revenue recognition timing differences between recurring and perpetual license sales inevitably means revenue and profit are compressed in the short term but contribute stronger and more predictable performance in the medium term as the book of ARR builds and improves forward visibility. 2022 saw an acceleration in ARR growth, including 13 existing perpetual customers converting to a SaaS model.

Following are the key financial performance indicators which we prioritize and track to run the business to achieve our stated business strategy. We are pleased with the positive development in these metrics, and I discuss them in more detail in the rest of my report.

Revenue metrics above are focused on our corporate software business, which in 2022 was primarily Accolade and associated consulting. TCV metrics quoted above include first year maintenance only for perpetual transactions, but the full multi-year committed value of any SaaS transactions. It is important to note the significant impact of the very large order with the US Navy, discussed further below, on TCV performance in 2022.

Trading Performance

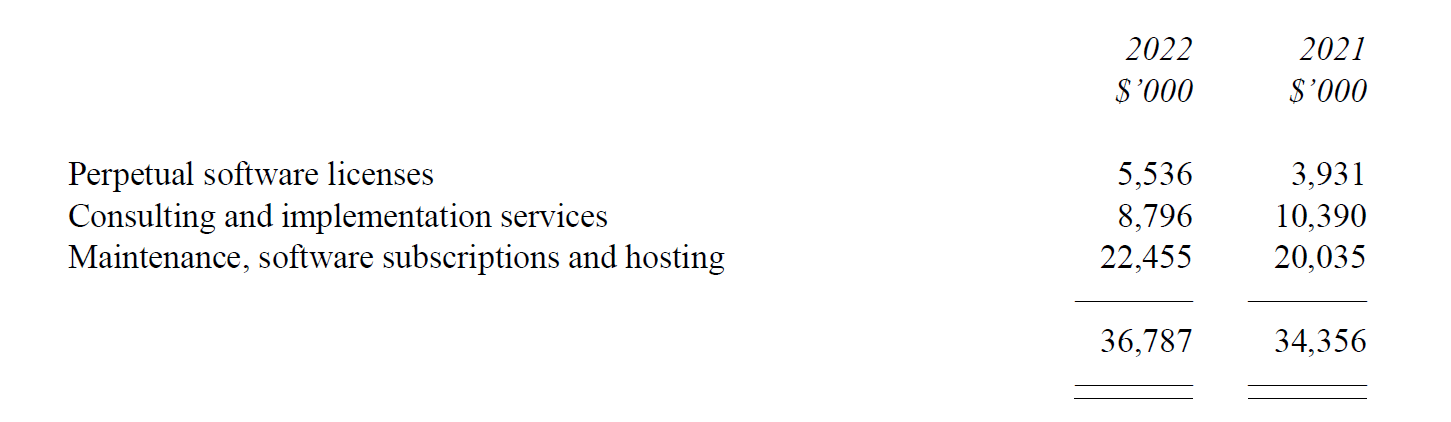

Overall revenue on a constant currency basis grew to $38.1m (2021: $34.4m). Due to strong US dollar appreciation against other currencies, our reported revenues were $36.8m. As set out in Note 4 to the financial statements, this comprises $5.5m of perpetual license (2021: $3.9m), $8.8m of consulting services (2021: $10.4m) and $22.5m of recurring SaaS and maintenance (2021: $20.0m). A comparatively quiet year for consulting following delivery of a substantial deployment with LG in 2021, was almost exactly offset by a stronger perpetual performance, largely driven by a contract signed with the US Navy. These events disguise the very real operational progress that is demonstrated by the growth in the recurring line and more importantly by the very strong growth in ARR by year end.

The US Navy is structured as an enterprise perpetual license together with long term maintenance and consulting commitments, with the payment profile spread evenly across the five-year period. Of the total deal value, approximately $4.1m was recognized as perpetual license fees in 2022 and the majority of this amount remains in receivables. A further $4.1m of maintenance, $2.7m of consulting and $0.3m of notional interest will be recognized over the five-year period. Even if the US Navy order were excluded, total TCV booked matched the previous year and the amount of SaaS nearly doubled. Our strategy is to accelerate and deepen this trend, and looking forward, we intend that all new license sales will be SaaS where possible. Conversions to SaaS increasingly include customers that already use Sopheon for hosting, who wish to access new SaaS only solutions such as Acclaim Projects, or to access new pricing models. In most cases, such orders are accompanied by an uplift in ARR as the customers expand the footprint of our software in their business. During the year, 13 customers moved from perpetual to SaaS, compared to six in 2021 and four in 2020. This pattern is underlined by the steady improvement in our NRR metric, which we are exposing for the first time this year.

A 2022 report by SaaS Capital indicates that median GRR and NRR for B2B vendors selling larger ticket enterprise software are 95% and 105% respectively. Sopheon performs well on both counts and shows a rising NRR trend, key to future growth dynamics.

Product, Seasonality and Geography

We continue to expect the sensitivity of revenue to calendarization to come down as our recurring revenue rises more steeply. However, due to the impact of the US Navy perpetual transaction this was not the case in 2022, with the second half of the year accounting for 58 percent of revenues (2021: 52 percent and 2020: 54 percent).

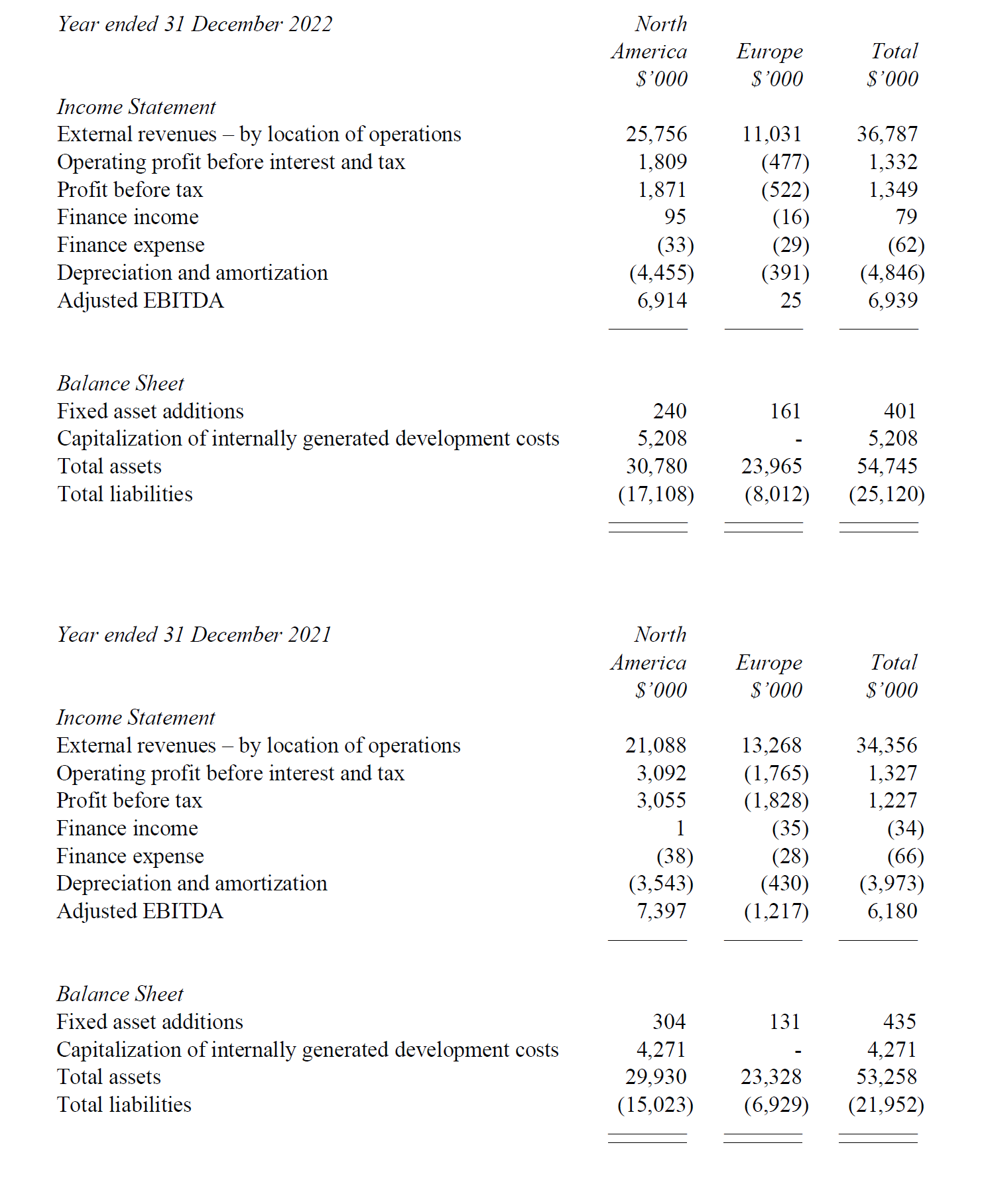

Revenues to customers in our core markets of North America and Europe, addressed by our direct sales teams, were 68 percent and 28 percent of total respectively (2021: 60% and 31%) again reflecting the impact of the Navy transaction. After relatively strong years for perpetual and consulting business in the Asia-Pacific region in 2020 and 2021, revenues outside our core regions fell back to 4 percent (2021: 9%). Our activities in the Pacific region continue to be managed through partnership channels. The revenue performance disguises some new SaaS signings in the territory, and we believe this region represents a growth opportunity for Sopheon.

The vast majority of revenue continues to come from the Accolade solution. However, as noted in the Chairman’s statement, Acclaim Projects was instrumental in concluding nine transactions in 2022, representing TCV signed in excess of $4m, and is playing a key role in our forward pipeline.

Gross Margin

Gross margin was 75 percent, compared to 73 percent in 2020, itself an increase over the year before. Gross margin is calculated after deducting the cost of our consulting organization – both payroll and subcontracted; costs and charges associated with our hosting activities, some license royalties due to OEM partners and costs and credits relating to certain indirect taxes. As before the change in margin last year was driven largely by the dynamics of our services organization. Lower revenues meant that consulting represents a smaller proportion of the overall margin mix; furthermore, not all departing staff were replaced.

Research and Development Expenditure

Headline R&D expense shows a large jump from $7.3m to $10.6m. However, this includes two non-operational items being (i) a $1.6m write down of previously capitalized costs, as further described below; and (ii) $0.6m in amortization of intangible assets added through the ROI Blueprints acquisition. Excluding these items, and factoring in the impact of capitalization, actual spend on R&D rose from $8.6m to $10.2m or from 25% to just under 28% of revenue. These are undoubtedly high by historic standards but reflect the major investment being made in the Acclaim product family alongside continuous improvements to Accolade as well as upward cost pressure. Average headcount in this area has remained broadly flat but has been supplemented extensively by subcontracted resources. Further details of capitalization and amortization of R&D expenses is described in Note 9.

Sopheon had embarked on the development of a next-generation platform for new cloud-based applications prior to our recent M&A transactions. In light of both acquisitions and other factors, the group revisited its original approach. As a consequence, a 100% impairment has been made against the capitalized costs associated with the cloud platform development, amounting to $1.6m, included in research and development expense and subtracted from adjusted EBITDA.

The amount of 2022 research and development expenditure that met the criteria of IAS 38 for capitalization was $5.2m (2021: $4.3m) offset by amortization charges of $3.4m (2021: $3.0m) and an impairment of $1.6m (2021: $nil). Capitalized costs in 2022 are largely attributable to the group’s investment in the Accolade 14.2, 14.3, 15.0 and 15.1 versions, as well as the more nascent Acclaim solutions, in particular the former ROI Blueprints offering, Acclaim Projects, which has had a positive impact on sales performance as noted above.

Other Operating Costs

Staff costs continue to represent over 80 percent of our cost base. Sopheon has a relatively mature and highly qualified blend of staff, reflecting the professional and intellectual demands of our chosen market. We ended 2022 with 178 staff and 18 full time offshore subcontracting resources (2021: 167 and 18). In addition, further R&D offshoring was conducted on a project deliverable basis, mainly to support one of the Acclaim solutions. Salary pressures continued during 2022, and we experienced significant staff churn as the “great resignation” impacts continued. While this contributed to cost savings against plan, the majority of leavers were replaced by year end, and we have seen this pressure fall off as we closed the year. Average headcount for the year was 172 compared to 165 the year before. In 2021 we had modified the corporate bonus scheme applicable to all non-sales staff in the company, adding a material element of ARR goal to our historical focus on Adjusted EBITDA; the ratio was increased in 2022, and was fully achieved. In spite of these upward pressures, compounded by increases in individual pay requirements in technical roles, staff costs were broadly flat year over year thanks mainly to the impact of the strong USD on the reported costs of our European employees.

Overall non-payroll costs increased by approximately $1m before exchange, interest, tax and depreciation. There were three main components of the increase being travel and related costs, expanding marketing programs, and infrastructure costs associated with the SaaS migration and Acclaim investments.

Taking a functional view, specific comments regarding consulting operations and research and development costs are noted above. Overall costs in the sales and marketing area look flat on a headline basis but this would have shown an increase due to higher marketing program spend, were it not for strong USD rates. Administration costs – which include infrastructure costs - have reduced by approximately $0.5m. This area includes all other overheads, office costs, regulatory and compliance costs, depreciation, and operational exchange movements, as well as the full impact of the notional charge for share option grants, which is allocated entirely to this caption. The majority of the fall came from exchange gains in Sopheon plc arising from GBP weakness, as well as lower rental costs due to reduced office footprints, offset by higher infrastructure costs.

With regard to foreign exchange, historically the group has aimed to incorporate a natural hedge through broadly matching revenues and costs within common currency entities, reducing the need for active currency management. In recent years this has become somewhat less balanced as our cost base has become increasingly USD driven, while revenues remain roughly two thirds USD and one third EUR/GBP. This has led to a build-up of EUR balances pending a reversal of the current USD strength.

Results and Corporate Tax

Adjusted EBITDA is a key indicator of the underlying performance of our business, commonly used in the technology sector. It is also a key metric for management and the financial analyst community. This measure is further defined and reconciled to profit before tax in Note 5. The combined effect of the revenue and cost performance discussed above has resulted in Sopheon’s adjusted EBITDA performance for 2022 rising to $6.9m, from $6.2m in 2021. The increase in profit before tax was more muted at just over $0.1m, due mainly to the incidence of higher amortization charges, rising to $1.3m (2021: $1.2m).

The tax charge of $2.2m (2021: $0.4m) reported in the income statement is made up of $1.9m (2021: $nil) of deferred tax movements arising mainly from the impact of legislation that has accelerated consumption of accumulated tax losses in the USA as further described in Note 7, and $0.3m (2021: $0.4m) of actual current tax. The movement in deferred tax has reduced the group’s recognized deferred tax asset to $0.6m (2021: $2.6m) of a potential total asset of $8.9m (2021: $11.7m).

Altogether this leads to a loss after tax of $0.9m (2021: profit of $0.8m). This has also resulted in loss per ordinary share on a fully diluted basis of 8.28 cents (2021: 7.47 cents profit).

Dividend

The board is pleased to maintain Sopheon’s dividend at 3.25 pence per share for the year ended 31 December 2022 (2021: 3.25p). We believe this level strikes the right balance between a business going through a complex SaaS transition, while still delivering positive revenue growth, cash generation and balance sheet strength. Subject to approval by the company’s shareholders at the annual general meeting scheduled for 8 June 2023, the dividend will be paid on 7 July 2023 with a record date of 9 June 2023.

Cash, Facilities and Assets

Net cash at 31 December 2022 amounted to $21.1m (2020: $24.2m). Approximately $4.7m was held in USD, $14.3m in EUR and $2.1m in GBP (2021: $5.6m, $15.4m and $3.2m respectively). The reduction in net cash is due to several factors:

- Cash utilization before financing was $0.9m (2021: generation of $3.9m) primarily reflecting a significant increase in receivables due to two factors. The majority of this increase can be explained by the extended payment terms associated with the US Navy enterprise agreement leading to $3.6m being included within the $4.1m contract asset recorded within receivables. Second, our recurring contract renewal dates concentrate in the final quarter of the year and the success in adding more SaaS agreements this year has further accentuated this issue, also leading to a higher trade receivable balance at year end than in the past.

- Investing activities including M&A, capitalized development costs and equipment was $0.3m higher than the year before, and net financing costs including dividends, interest and share issue proceeds was $0.2m higher.

- As noted above Sopheon holds considerable EUR as well as GBP cash balances, which due to currency movements, fell in value by approximately $1m in USD terms over the course of the year.

The group has no debt (excluding notional debt from the adoption of IFRS 16). However, we maintain our good relationships with our financing partners, with potential established for funding arrangements in connection with corporate activity if required.

Intangible assets stood at $13.1m (2021: $12.0m) at the end of the year. This includes (i) $8.3m being the net book value of capitalized research and development (2021: $8.1m) (ii) the net book value of acquired technology and IPR of $1.7m arising on the acquisition of ROIB (2021: $2.3m); and (iii) an additional $3.1m (2021: $1.6m) being goodwill arising on acquisitions, including $0.6m for ROIB arising in 2021 and $1.5m for Solverboard arising in 2022.

As stated above in our discussion of research and development costs, capitalization and amortization have historically been broadly in balance; however, recently capitalization has accelerated as we have expanded our range of product offerings, and amortization has yet to catch up. Nevertheless, due to the $1.6m impairment noted above booked against the capitalized costs associated with internal cloud platform development prior to our recent acquisitions, in 2022 the net total of capitalization, amortization and impairment was broadly in balance.

With respect to the acquisition of Solverboard, we have estimated approximately 29 percent of the contingent consideration will become payable during the earnout period, resulting in a total net acquisition cost being recorded of $1.5m which is all treated as goodwill.

IFRS 16 requires lessees to recognize a lease liability that reflects future lease payments and a "right-of-use asset" in all lease contracts within scope, with no distinction between financing and operating leases. This has resulted in net book value of right-of-use assets of $0.5m (2021: $0.8m) and corresponding lease liabilities of $0.5m (2021: $0.8m) at 31 December 2021. Notional amortization and interest charges in connection with the above recognized in the income statement were approximately $0.5m (2021: $0.7m).

Consolidated net assets at the end of the year stood at $29.6m (2021: $31.3m), a decrease of $1.7m and including net current assets of $15.6m (2021: $15.7m).

1. Basis of Preparation

The financial information set out in this document does not constitute the Company's statutory accounts for the years ended 31 December 2021 or 2022. Statutory accounts for the year ended 31 December 2022, which were approved by the directors on 22 March 2023, have been reported on by the Independent Auditors. The Independent Auditors' Reports on the Annual Report and Financial Statements for each of 2021 and 2022 were unqualified, did not draw attention to any matters by way of emphasis, and did not contain a statement under 498(2) or 498(3) of the Companies Act 2006.

The Annual Report (including the statutory financial statements) for the year ended 31 December 2021 have been filed with the Registrar of Companies. The Annual Report (including the statutory financial statements for the year ended 31 December 2022) will be delivered to the Registrar in due course, and are available from the Company's registered office at Dorna House One, Guildford Road, West End, Surrey GU24 9PW and are available today from the Company's website at www.sopheon.com/financial-reports/.

The financial information set out in these results has been prepared using the recognition and measurement principles of UK adopted International Accounting Standards in accordance with the requirements of the Companies Act 2006. The accounting policies adopted in these results have been consistently applied to all the years presented and are consistent with the policies used in the preparation of the financial statements for the year ended 31 December 2021, except for those that relate to new standards and interpretations effective for the first time for periods beginning on (or after) 1 January 2022. There are deemed to be no new standards, amendments and interpretations to existing standards, which have been adopted by the Group that have had a material impact on the financial statements. Approximately two-thirds of the Group’s revenue and operating costs are denominated in US Dollars and accordingly the Group’s financial statements have been presented in US Dollars.

2. Going Concern

The consolidated financial statements have been prepared on a going concern basis. The directors have at the time of approving the financial statements, a reasonable expectation that the company has adequate resources to continue in operational existence for the foreseeable future.

The Covid-19 pandemic, Brexit and the war in Ukraine have so far had limited impact on the business, and the board believes that the business is able to navigate through the continued challenges of these events due to the strength of its customer proposition, statement of financial position and the net cash position of the group. However, these conditions continue to create uncertainty and have had a widespread impact economically, with potential for causing delays in contract negotiations and/or cancelling of anticipated sales and an uncertainty over cash collection from certain customers. As a consequence, the group has carried out detailed forecast stress testing in order to consider how much forecasts have to reduce by in order to cause cash constraints, and also to consider the likelihood of this scenario occurring. This assessment has also included the group’s actual cash holdings as of the date of the approval of the financial statements and financing alternatives available to the group. Overall, these cash-flow forecasts, which cover a period of at least 12 months from the date of approval of the financial statements, foresee that the group will be able to operate within its existing facilities. Nevertheless, there is a risk that the group will be impacted more than expected by reductions in customer confidence if global economic sentiment deteriorates. If sales and settlement of existing debts are not in line with cash flow forecasts, the directors have the ability to identify cost savings if necessary, to help mitigate the impact on cash outflows.

Having assessed the principal risks and the other matters discussed in connection with the going concern statement, the directors have a reasonable expectation that the group has adequate resources to continue in operational existence for the foreseeable future and settle liabilities as they fall due. For these reasons, they continue to adopt the going concern basis of accounting in preparing the financial information.

3. Segmental Analysis

All of the Group’s revenue in respect of the years ended 31 December 2022 and 2021 derived from the design, development and marketing of software products with associated implementation and consultancy services, as more particularly described in the Chairman’s statement. The business is seen as one cash generating unit and operates as a single operating segment. For management purposes, the Group is organized geographically across two principal territories, North America and Europe. Information relating to this geographical split is outlined below.

The information in the following table relates to external revenues location of operations. Inter-segment revenues are priced on an arm’s length basis.

Revenues attributable to customers in North America in 2022 amounted to $24,953,000 (2021: $20,434,000). Revenue attributable to customers in the rest of the world amounted to $11,834,000 (2021: $13,922,000) of which $10,468,000 (2021: $10,765,000) was attributable to customers in Europe.

Revenues attributable to customers in North America in 2022 amounted to $24,953,000 (2021: $20,434,000). Revenue attributable to customers in the rest of the world amounted to $11,834,000 (2021: $13,922,000) of which $10,468,000 (2021: $10,765,000) was attributable to customers in Europe.

4. Revenue from contracts with customers

All of the Group’s revenue in respect of the years ended 31 December 2022 and 2021 derived from continuing operations and from the design, development and marketing of software products with associated implementation and consultancy services. The following table provides further disaggregation of revenue in accordance with the IFRS 15 requirement to depict how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

Perpetual licenses are recognized at a point in time. Consulting and implementation services, and maintenance, subscription and hosting services, are recognized over time.

5. Adjusted EBITDA

Adjusted EBITDA, which is a company specific measure, is defined as earnings before interest, tax, depreciation, amortization and employee share-based payment charges is an important measure, since it is widely used by the investment community. It is calculated by deducting net interest receivable of $17,000 (2021: adding back net interest payable of $100,000) and adding back depreciation and amortization charges amounting to $4,846,000 (2021: $3,974,000) and employee share-based payment charges of $761,000 (2021: $880,000) to the profit before tax of $1,349,000 (2021: $1,227,000).

6. Share-Based Payments

In accordance with IFRS 2 Share based Payments, an option pricing model has been used to work out the fair value of share options granted by the Group, with this being charged to the income statement over the expected vesting period and leading to a charge of $761,000 (2021: $880,000). Where an option vests in multiple instalments, each instalment is treated as a separate grant with its own vesting period. The entire expense is recognized within administrative expenses.

7. Income Tax

The income tax expense of $2,226,000 (2021: $410,000) comprises current tax expense of $294,000 and deferred tax expense of $1,932,000 (2021: Nil). The current tax expense represents German corporation tax payable by Sopheon GmbH and US state taxes payable by the Group’s US subsidiaries.

The movement in the deferred tax asset reflects amendments to US Code Section 174 which now requires taxpayers to charge their research expenditures and software development costs to a capital account. Capitalized costs are required to be amortized over five years (15 years for foreign costs). This has led to a significant acceleration of the utilization of US unrelieved trading losses in 2022, and also resulted in a change in timing difference arising from the capitalization and transfer of development investments.

At 31 December 2022, tax losses estimated at $46.2m (2021: $54.2m) were available to carry forward by the Sopheon group, arising from historical losses incurred. These losses have given rise to a deferred tax asset of $1.4m (2021: $2.6m), offset by a deferred tax liability arising from capitalization of internally generated development costs of $0.7m (2021: $nil) and a further potential deferred tax asset of $8.7m (2021: $9.1m), based on the tax rates currently applicable in the relevant tax jurisdictions. Of these tax losses, an aggregate amount of $8.1m, representing $1.7m of the potential deferred tax asset (2021: $8.7m and $1.8m respectively) represents pre-acquisition tax losses of Alignent Software, Inc. The future utilization of these losses may be restricted under Section 382 of the US Internal Revenue Code, whereby the ability to utilize net operating losses arising prior to a change of ownership is limited to a percentage of the entity value of the corporation at the date of change of ownership.

8. Earnings per Share

The calculation of basic earnings per ordinary share is based on a loss of $877,000 (2021: profit of $817,000), and on 10,594,000 (2021: 10,442,000) ordinary shares, being the weighted average number of ordinary shares in issue during the year. The profit attributable to ordinary shareholders and the weighted average number of shares for the purpose of calculating the diluted earnings per ordinary share are the same as those used for calculating the basic earnings per share for 2022. This is because the 840,887 share options to subscribe for ordinary shares would have the effect of reducing the loss per share.

9. Intangible Assets

In accordance with IAS 38 Intangible Assets, certain development expenditure must be capitalized and amortized based on detailed technical criteria, rather than automatically charging such costs in the income statement as they arise. This has led to the capitalization of $5,207,000 (2021: $4,271,000), and amortization of $3,386,000 (2021: $2,997,000) during the year.

On 18 May 2022 the group announced the acquisition of Solverboard, a cloud-based business, based in the UK and specializing in the front-end of innovation management. Initial consideration comprised £500,000 in cash and £250,000 in shares issued at £6 per share. An additional, contingent deferred earn-out of up to £1.55 million may be payable over two years, linked to Annual Recurring Revenue ("ARR") targets. The contingent deferred consideration may be satisfied by the issue of up to £900,000 in shares issued at £6 per share, with the balance in cash. The initial consideration of £750,000 ($931,000) has been allocated to goodwill. The contingent deferred consideration has been assessed at a fair value of £445,000 ($549,000) and has also been allocated to goodwill.

Prior to the acquisitions of ROI Blueprints (in December 2021) and of Solverboard, the group had embarked on its own development of a next-generation platform for new cloud-based applications. In the light of both acquisitions and other factors, the group has revisited its original approach. As a consequence, a full impairment provision has been made against capitalized historic development costs associated with the group’s own cloud platform development, amounting to $1.6m, which is included in research and development expense.

10. Cautionary Statement

Sopheon has made forward-looking statements in this press release, including statements about the market for and benefits of its products and services; financial results; product development plans; the potential benefits of business relationships with third parties and business strategies. These statements about future events are subject to risks and uncertainties that could cause Sopheon's actual results to differ materially from those that might be inferred from the forward-looking statements. Sopheon can make no assurance that any forward-looking statements will prove correct.