Sopheon, the international provider of software and services for Enterprise Innovation Management solutions, announces its unaudited half-yearly financial report for the six months ended 30 June 2022 (“H1”) together with a business review and outlook statement for the second half of the year.

Highlights:

-

Full year 2022 revenue visibility1 is now at an encouraging $34.1m (last year at this time: $31.2m). This includes revenue to be recognized in 2022 from the recently announced US Navy agreement concluded in July. Year to date TCV2, also including the US Navy agreement is now at $22m, almost equal to 2021’s full year TCV and over 60% higher than at this time last year.

-

H1 revenue was $15.7m compared to $16.5m in H1 2021, with materially more multi-year SaaS versus perpetual license and service contracts leading to deferral in relative revenue recognition. 8 new customers were signed, and all were SaaS in line with our transition strategy.

-

SaaS ARR2 of $9.3m at 30 June (30 June 2021: $7.6m, 31 Dec 2021 $7.9m) representing 22% year over year growth. Total ARR including SaaS and maintenance of $21.9m at 30 June (30 June 2021: $19.5m, 31 Dec 2021 $20.8m) representing 12% year over year growth. Gross ARR retention for the six months at 98% (H1 2021: 97%).

-

Currency movements have had a material impact on reported performance due to the sharp rise in US dollar against Euro and Sterling in 2022. At prior year currency rates, H1 2022 revenue would have been $16.2m. Similarly, at 2021 currency rates SaaS ARR would have been $9.6m and total ARR $22.5m at 30 June – constant currency growth of 26% and 15% respectively.

-

Adjusted EBITDA4 of $2.9m (H1 2021: $2.8m).

-

Net cash at 30 June of $23.5m after funding M&A and dividends (30 June 2021: $24.1m) and the Group is debt free.

-

Acquisition of Solverboard for initial consideration of $0.9m, a UK based SaaS business specializing in the front-end of innovation management – a second transaction less than six months after the acquisition of ROI Blueprints, a US based SaaS business specializing in project management.

Sopheon’s Executive Chairman, Andy Michuda said: “I am pleased to report revenue visibility already approaching 2021’s full year results with most of H2 still ahead of us. We continue to show good ARR growth especially in SaaS, supported by high levels of retention. Commercial traction is also building, with both a faster pace of net new sales and the signing of the largest single deal in our history with the US Navy – underpinning future performance. Our strategic initiatives are broadly on track and in a time of continued global uncertainty, our substantial cash reserves provide additional confidence for execution both in terms of organic initiatives, and to move quickly if further acquisition opportunities arise. Recent acquisitions have rounded out our product roadmap, and we are on the cusp of introducing a new go-to-market approach that significantly expands our addressable market and competitive advantage. This is one of the most exciting periods in my time at Sopheon, with both momentum and opportunity in equal measure.”

For further information contact:

| Andy Michuda, Executive Chairman Arif Karimjee, CFO |

Sopheon plc | + 44 (0) 1276 919 560 |

| Carl Holmes / Edward Whiley (corporate finance) Alice Lane / Sunila de Silva (ECM) |

finnCap Ltd | + 44 (0) 20 7220 0500 |

About Sopheon

Sopheon (LSE: SPE) partners with customers to provide complete enterprise innovation management solutions including software, expertise, and best practices, that enable them to achieve exceptional long-term revenue growth and profitability. Sopheon’s Accolade solution provides unique, fully-integrated coverage for the entire innovation management and new product development lifecycle, including strategic innovation planning, roadmapping, idea and concept development, process and project management, portfolio management and resource planning. Sopheon’s solutions have been implemented by over 250 customers with over 60,000 users in over 50 countries. Sopheon is listed on AIM, operated by the London Stock Exchange.

1 Revenue visibility is defined in Note 5.

2 TCV is total contract value of sales bookings in the period

3 ARR is annualized recurring revenue at a point in time

4 Adjusted EBITDA is defined in Note 3

Chairman's Statement

Trading Performance

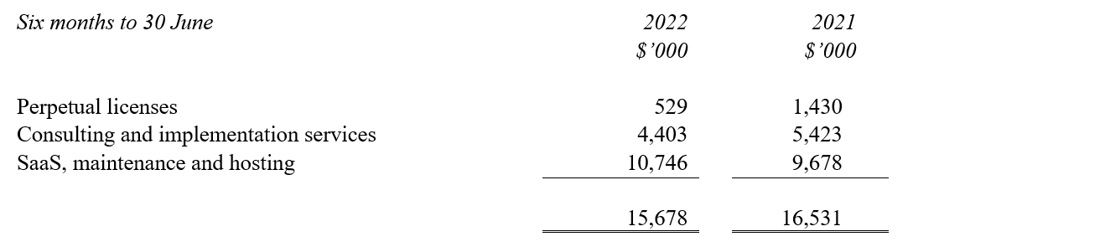

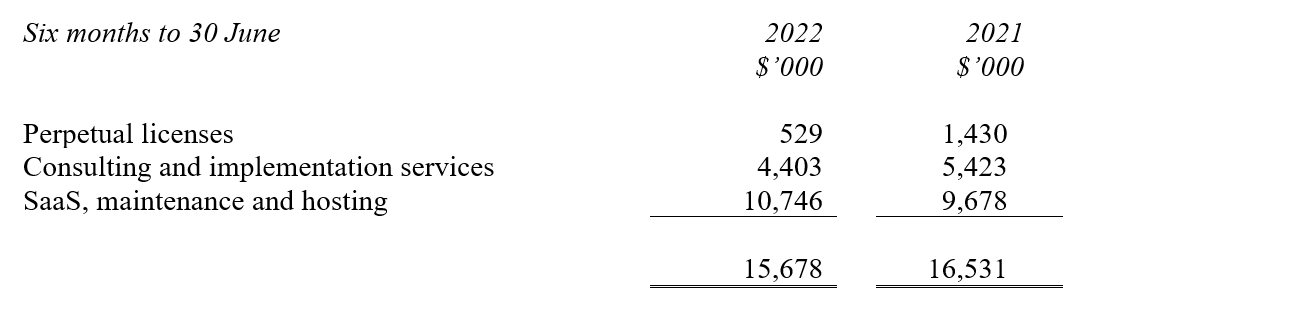

Revenue in the first half of 2022 was $15.7m compared to $16.5m in the first half of 2021. This dip does not reflect the underlying performance of the business which is delivering on our strategy of prioritizing SaaS sales and associated ARR, as opposed to one-off perpetual license sales and consultancy sales. The progress and impact of this transformation is clear in the make-up of first half revenues compared to the prior year and summarized in the table below, extracted from Note 3:

The rise in total recurring revenue is reflected in ARR growing from $19.5m a year ago to $21.9m at 30 June 2022, an increase of 12%. Focusing on the strategic subsection of ARR relating to SaaS and hosting business, this rose from $7.6m to $9.3m – an increase of 22%. At 31 December 2021, total ARR was $20.8m and SaaS ARR was $7.9m. Retention levels continue to improve with our ARR gross retention rate at 98% year to date, up from 97% at this time last year. During the six-month period we also added 8 new customers, more than double last year’s H1 count. Average deal size per initial net-new sale was consistent with our long-term benchmark of approximately $0.4m.

Currency movements have had a material impact on reported performance due to the sharp rise in US dollar against Euro and Sterling in 2022. At prior year currency rates, H1 2022 revenue would have been $16.2m. Similarly, at 2021 currency rates SaaS ARR would have been $9.6m and total ARR $22.5m at 30 June – constant currency growth of 26% and 15% respectively.

As last year, all our new customers opted for SaaS, underpinning our move to the recurring revenue model. We expect a declining level of perpetual business over the next few years, primarily from existing accounts signing extension orders. Our consulting business will also continue to generate project based billable revenue which remains an important element of our revenue goals during the transition journey. Just under half our customers are still licensed under an on-premise perpetual model and we continue to work with them to transition to SaaS through our cloud lift program, which will take some time. We have also had initial sales successes for ROI Blueprints, acquired at the end of 2021, to both new and existing customers. As anticipated, the ROI Blueprints software has assisted with our competitive position in pursuing new customers. Revenue from new cloud products, including Solverboard acquired in May 2022, is expected to start to contribute in the second half of the year.

As separately announced last week, expanding on our previous partnership with NAVSEA we were delighted to conclude a five-year, $11.2m enterprise agreement with the US Navy in July, the largest single booking in our history which paves the way for further expansion of our government business. This transaction is structured as an enterprise perpetual license together with long term maintenance and consulting commitments, with the payment profile spread broadly evenly across the five-year period. Of the total deal value, approximately $4.1m will be recognized as perpetual license fees in the current year. The balance of $4.1m of maintenance, $2.7m of consulting and $0.3m of notional interest will be recognized over the five-year period.

In addition to the US Navy agreement, since the end of June we have continued to book business from new and existing customers, and we are pleased to report that revenue visibility today stands at $34.1m compared to $31.2m at this time last year. Today and including the US Navy agreement, total TCV of sales closed year to date is over $22m, more than 60% higher than this time last year.

Margin, Operations and Results

Gross margin for the period held at 71% (2021: 71%). Direct costs include costs for license and support for certain OEM components of our solution, costs of our hosting operations, and movements in indirect taxes; but the main component is the cost of our delivery and support teams, and associated subcontractors.

Competition for staff during the post-pandemic era has become increasingly fierce, and costs of employment continue to accelerate especially in the technical area. This has been further pressured by the high-inflation environment we currently find ourselves in. While we have been successful in bringing in a substantial number of excellent new recruits, we have also experienced some staff turnover. Accordingly, average headcount for the first half of the year was 171 (H1 2021: 169). We have continued to increase subcontracting especially in the product development area where we continue to leverage growing partnerships with India based firms. Underlying overhead costs are approximately $0.2m higher overall, with a reduced incentive provision and exchange gains recorded in Sterling books offset by higher costs in research and development, marketing expense, IT and travel. The areas that have increased all reflect focus on strategic or commercial priorities. Much of the higher research development costs were capitalized, however, this was matched by higher amortization and impairment charges. From a functional perspective this is reflected in lower headline numbers for sales and administration, but higher in research and development.

Prior to entering into M&A activities, Sopheon had embarked on the development of a next-generation platform for new cloud-based applications. In light of both acquisitions and other factors, the Group is revisiting its original approach. As a consequence, a 50% impairment provision has been made against the capitalized costs associated with the cloud platform development, amounting to $0.8m, included in research and development expense. A full evaluation will be completed by year end.

Loss before tax reported for the half-year period was $0.8m (H1 2021: profit of $0.5m). This result includes net interest, depreciation and amortization, the impairment charge referenced above, and share-based payment costs totaling $3.7m (H1 2021: $2.3m). The Adjusted EBITDA result for the first half of 2022, which does not include these elements, was broadly flat at $2.9m (H1 2021: $2.8m). Provision has been made for approximately $0.3m in tax, primarily for German corporation tax where we do not benefit from historic losses (H1 2020: $0.1m), giving a final loss after tax of $1.2m compared to a profit of $0.4m the year before.

Balance Sheet

Net assets at 30 June 2022 stood at $29.3m (30 June 2020: $30.8m / 31 December 2021: $31.3m), with cash at the end of the period standing at $23.5m (30 June 2020: $24.1m / 31 December 2021: $24.2m). We note that the fall in these key balance sheet items is after funding initial consideration for two acquisitions, the dividend payments made in both 2021 and 2022, and the significant rise in the US dollar compared to Euro and Sterling in which currencies the Group has substantial balances. The Group has no borrowings. Intangible assets at 30 June 2021 stood at $13.2m (30 June 2021: $8.7m / 31 December 2021: $12.0m). The total includes (i) $8.6m being the net book value of capitalized research and development (30 June 2021: $7.6m) and (ii) $4.5m (30 June 2021: $1.0m) being the net book value of acquired intangible assets and goodwill. This includes $2.5m in respect of ROI Blueprints, and $0.9m in respect of Solverboard as further detailed below.

The acquisition of Solverboard was structured as a business and asset purchase. Initial consideration comprised £500,000 in cash and £250,000 in shares issued at £6 per share. An additional, contingent deferred earn-out of up to £1.55 million is payable over the next two years, linked to ARR targets and to be satisfied by up to £900,000 in shares issued at £6 per share, with the balance in cash. As at the date of this report, due to the early-stage nature of the Solverboard business and post-acquisition activities, no value has been ascribed for the earn-out and accordingly, goodwill of $0.9m has been provisionally recorded. This assessment will be refined and revisited at the end of the year.

Strategic Progress

As described in our 2021 annual report our growth plans are built around an integrated three-point strategy, and we continue to make significant progress in all areas:

- SaaS / ARR growth – As noted earlier in this report, we continue to build commercial traction in our transition to a recurring revenue model, with all new customers this year being SaaS, along with conversions of our existing perpetual base leading to strong SaaS ARR growth over 20%. In addition, both recent acquisitions are SaaS businesses.

- Fill out the product roadmap – We have considerably strengthened the breadth of the Sopheon offering through the acquisitions of ROI Blueprints and Solverboard, which address project and idea problem solving respectively in a much deeper way than Accolade which has a product and portfolio focus. In parallel we have continued and accelerated the pace of development for Accolade itself, with four releases in the last 12 months. As noted above we also embarked on the development of cloud-native, multi-tenant applications in specific innovation related areas encompassing product, project and idea problem solving. The first of these is already in market testing. The other two are based on ROI Blueprints and Solverboard respectively and are at different stages of their market launch journeys.

- New go-to-market strategies to expand market reach – Accolade has historically been sold to major corporations using an enterprise sale, vertical market approach focused primarily on food and beverage, other consumer products, chemical, defense and industrial manufacturing. Solving the innovation governance needs of corporations with Accolade, in such markets, will remain a core focus and growth driver for Sopheon. In support of expanding our addressable market and faster growth, we now see a major opportunity to expand distribution with new cloud-native applications directly targeting individual contributors within the corporate setting (also known as the product led or PLG approach). Such users will in turn feed our enterprise sales teams, ultimately offering lead generation for Accolade. In addition, marketing investments have been stepped up in anticipation of this new channel, as well as building the Accolade pipeline. Our market reach and engagement metrics continue to advance accordingly.

Sopheon’s vision, strategy and strong performance is recognized by key industry analysts with our inclusion in 14 current Gartner reports – 12 since August 2021 – including their hype cycles for life science discovery research, consumer goods and strategic portfolio management - as well as several earlier Gartner and Forrester reports from 2020 and earlier in 2021.

Outlook

I am pleased to report revenue visibility already approaching 2021’s full year results with most of H2 still ahead of us. We continue to show good ARR growth especially in SaaS, supported by high levels of retention. Commercial traction is also building, with both a faster pace of net new sales and the signing of the largest single deal in our history with the US Navy – underpinning future performance. Our strategic initiatives are broadly on track and in a time of continued global uncertainty, our substantial cash reserves provide additional confidence for execution both in terms of organic initiatives, and to move quickly if further acquisition opportunities arise. Recent acquisitions have rounded out our product roadmap, and we are on the cusp of introducing a new go-to-market approach that significantly expands our addressable market and competitive advantage. This is one of the most exciting periods in my time at Sopheon, with both momentum and opportunity in equal measure.

| Andy Michuda Executive Chairman |

23 August 2022 |

Notes to the Consolidation Financial Statements

1. General Information

Sopheon plc is a company domiciled in England. The interim financial information of the Company for the six months ended 30 June 2022 comprise the Company and its subsidiaries (together referred to as the "Group").

The Board of Directors approved this interim report on 23 August 2022.

2. Principal Accounting Policies

Basis of preparation and accounting policies

These condensed consolidated financial statements have been prepared in accordance with UK adopted international accounting standards in accordance with the requirements of the Companies Act 2006. They do not include all disclosures that would otherwise be required in a complete set of financial statements and should be read in conjunction with the 31 December 2021 Annual Report. The financial information for the half years ended 30 June 2022 and 30 June 2021 does not constitute statutory accounts within the meaning of Section 434 (3) of the Companies Act 2006 and both periods are unaudited.

The annual financial statements of Sopheon plc (‘the Group’) are prepared in accordance with international accounting standards in conformity with the requirements of the Companies Act 2006. The statutory Annual Report and Financial Statements for 2021 have been filed with the Registrar of Companies. The Independent Auditors’ Report on the Annual Report and Financial Statements for the year ended 31 December 2021 was unqualified, did not draw attention to any matters by way of emphasis and did not contain a statement under 498(2) - (3) of the Companies Act 2006.

The Group has applied the same accounting policies and methods of computation in its interim consolidated financial statements as in its 31 December 2021 annual financial statements, except for those that relate to new standards and interpretations effective for the first time for periods beginning on (or after) 1 January 2022 and will be adopted in the 2022 financial statements. There are deemed to be no new and amended standards and/or interpretations that will apply for the first time in the next annual financial statements that are expected to have a material impact on the Group.

Going Concern

The consolidated financial statements have been prepared on a going concern basis. In reaching their assessment, the directors have considered a period extending at least 12 months from the date of approval of this half-yearly financial report. As is widely understood and discussed in more detail in note 9 below, the COVID-19 global pandemic followed by the war in Ukraine have had widespread economic impacts, with potential for causing delays in contract negotiations and/or cancellation of anticipated sales, as well as uncertainty over cash collection from certain customers. The Group proved to be resilient in the face of such pressures; however, the directors have continued to perform detailed forecast stress testing, assessing how much forecasts would need to reduce by in order to cause cash constraints, and also to consider the likelihood of this scenario occurring. The results of this analysis continue to give the directors comfort that a scenario which would cause such cash restrictions is remote, and therefore not a realistic outcome to consider. This assessment has included the Group’s actual cash holdings as of the date of the approval of this report, and the financing alternatives available. The Group’s cashflows are projected to be at a sufficient level to allow the Group to meet its obligations and liabilities as they fall due. Thus, the directors of the Company continue to adopt the going concern basis of accounting in preparing the financial statements.

Revenue Recognition

Revenue is measured at the fair value of the consideration received or receivable and represents amounts receivable for goods and services provided in the normal course of business, net of discounts and sales-related taxes. Sales of perpetual software licenses are recognized once no significant obligations remain owing to the customer in connection with such license sale. Such significant obligations could include giving a customer a right to return the software product without any preconditions, or if the Group is unable to deliver a material element of the software product by the balance sheet date. Revenues relating to software subscription, maintenance, and hosting agreements are deferred creating a contract liability at the period end, and recognized evenly over the term of the agreements, due to the customer simultaneously receiving and consuming the benefits of the contractual performance obligation over that term. Revenues from implementation and consultancy services are recognized as the services are performed, or in the case of fixed price or milestone-based projects, on a percentage basis as the work is completed and any relevant milestones are met, using latest estimates to determine the expected duration and cost of the project. Based on stage of completion and billing arrangement, either a contract asset or a contract liability is created at the period end. Where a sales contract involves multiple service obligations, the allocation of the transaction price is performed proportionally based on the standalone selling price for each obligation. The way in which management assigns the selling price to each separate performance obligation is based on the cost of satisfying the performance obligation plus an appropriate margin based on experience of standalone sales.

Deferred Tax

Deferred tax is recognized on differences between the carrying amounts of assets and liabilities in the financial statements and the corresponding tax bases used in the computation of taxable profit, and is accounted for using the balance sheet liability method. Deferred tax liabilities are generally recognized for all taxable temporary differences. Deferred tax assets are recognized only to the extent that the level and timing of taxable profits can be measured and it is probable that these will be available against which deductible temporary differences can be utilized. Deferred tax is calculated at tax rates that have been enacted or substantively enacted at the balance sheet date, and that are expected to apply in the period when the liability is settled or the asset realized. Deferred tax is charged or credited to profit or loss, except when it relates to items charged or credited directly to equity, in which case the deferred tax is also dealt with in equity.

Internally Generated Intangible Assets (Research and Development Expenditure)

Development expenditure on internally developed software products is capitalized if it can be demonstrated that:

- it is technically feasible to develop the product;

- adequate resources are available to complete the development;

- there is an intention to complete and sell the product;

- the Group is able to sell the product;

- sales of the product will generate future economic benefits; and

- expenditure on the product can be measured reliably.

Development costs not satisfying the above criteria and expenditure on the research phase of internal projects are recognized in the income statement as incurred. Capitalization of a particular activity commences after proof of concept, requirements and functional concept stages are complete. Capitalized development costs are amortized over the period over which the Group expects to benefit from selling the product developed. This has been estimated to be four years from the date of code-finalization of the applicable software release. The amortization expense in respect of internally generated intangible assets is included in research and development costs.

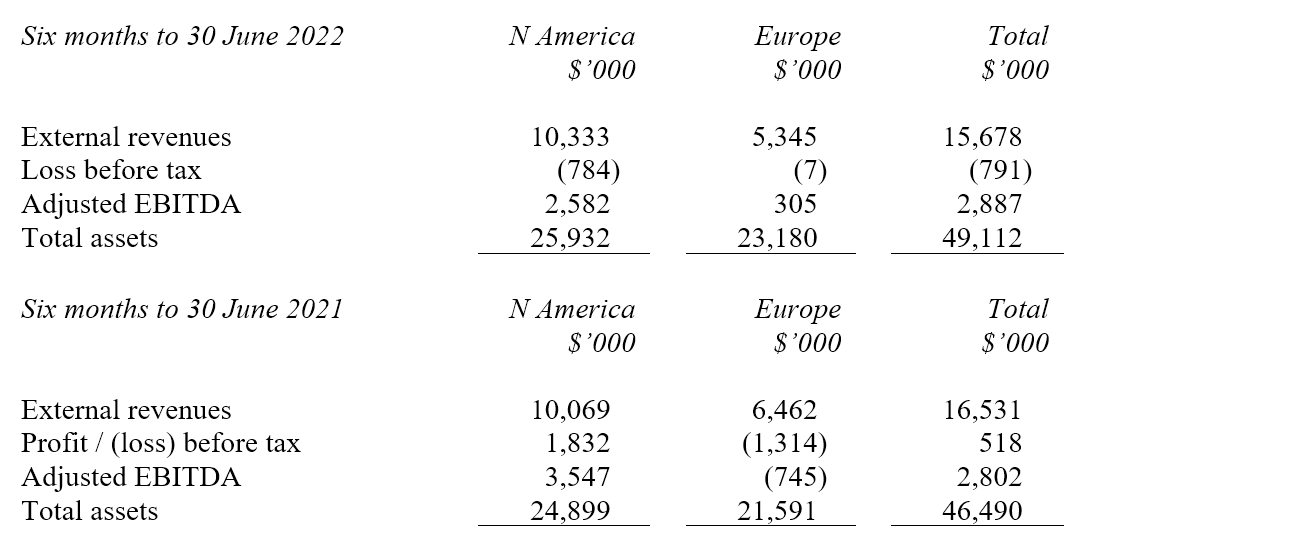

3. Revenue, Segmental Analysis and EBITDA

All of the Group’s revenues in respect of the six month periods ended 30 June 2022 and 30 June 2021 derived from the design, development and marketing of software products with associated implementation and consultancy services. The following table disaggregates revenue in accordance with the IFRS 15 requirement to depict how the nature, amount, timing and uncertainty of revenue and cash flows are affected by economic factors.

For management purposes, the Group is organized across two principal geographic operating segments, as used in the Group’s last annual financial statements. The first segment is North America, and the second Europe. Information relating to these two segments is given below.

Adjusted EBITDA is arrived at after adding back net finance costs, depreciation, amortization, impairment and share-based payment expense amounting to $3,678,000 (2021: $2,284,000) to the loss before tax. Details of these amounts are set out in the reconciliation of operating cash flows before movement in working capital, in the consolidated cash flow statement. Adjusted EBITDA is a key indicator of the underlying performance of our business, commonly used in the technology sector. It is also a key metric for management and the financial analyst community.

All information provides analysis by location of operations. The majority of revenue from customers in the rest of the world is recorded in the Europe segment. Loss/profit before tax and EBITDA are stated after adjusting for an estimate for intra-group charges.

4. (Loss) / Earnings Per Share

The calculation of basic (loss) / earnings per ordinary share is based on the loss of $1,050,000 (2021: earnings of $370,000) and on 10,564,081 ordinary shares (2021: 10,376,214) being the weighted average number of ordinary shares in issue during the period.

For the purpose of calculating the diluted earnings per ordinary share, any options to subscribe for Sopheon shares at prices below the average share price prevailing during the period are treated as exercised at the later of 1 January 2022 or the grant date. The treasury stock method is then used, assuming that the proceeds from such exercise are reinvested in treasury shares at the average market price prevailing during the period. The diluted number of shares used at 30 June 2022 is 10,682,876 (2021: 10,698,799). However, with respect to 30 June 2022, since this would have the effect of reducing the loss per ordinary share it is not dilutive and is therefore ignored.

5. Revenue Visibility

Revenue visibility at any point in time comprises revenue expected during the current year from (i) closed license orders, including those which are contracted but conditional on acceptance decisions scheduled later in the year; (ii) contracted services business delivered or expected to be delivered in the year; and (iii) recurring maintenance, hosting and license subscription streams. The visibility calculation does not include revenues from new sales opportunities expected to close later in the year.

6. Intangible Assets & Goodwill

Certain development expenditure is required to be capitalized and amortized based on detailed technical criteria (note 2) rather than automatically charging such costs in the income statement as they arise. This has led to the capitalization of $2,934,000 (2021: $2,166,000), and amortization of $1,541,000 (2021: $1,443,000) during the period. In addition, a 50% impairment provision has been made against the capitalized costs associated with the cloud platform development, amounting to $814,000 (2021: $nil). Amortization of $281,000 (2021: $nil) has also been charged in respect of technology and intellectual property rights acquired pursuant to the acquisition of ROI Blueprints LLC in 2021. A provisional amount of goodwill of $931,000 has been recorded in respect of the acquisition of the business and assets of Solverboard, to be revisited and retrospectively adjusted at year end, to reflect new information obtained about facts and circumstances that existed as of the acquisition date.

7. Taxation

The tax charge reflects certain US state taxes and German corporate taxes. At 30 June 2022, income tax losses estimated at $51m (2021: $54m) were available to carry forward by the Group, arising from historic losses incurred at the US federal level and also in the UK and the Netherlands. These losses have given rise to a recognized deferred tax asset of $2.6m (2021: $2.6m) and a further, but currently unrecognized, potential deferred tax asset of $8.8m (2021: $10.1m), based on the tax rates currently applicable in the relevant tax jurisdictions. An aggregate $9m (2021: $9m) of these tax losses are subject to restriction under section 392 of the US Internal Revenue Code, whereby the ability to utilize net operating losses arising prior to a change of ownership is limited to a percentage of the entity value of the corporation at the date of change of ownership. In addition to income taxes, the Group is also subject to sales and value added tax in the various jurisdictions in which it operates.

8. Dividend

The Board proposed a final dividend in respect of the year ended 31 December 2021 of 3.25p per share (2020: 3.25p per share). This was approved by the shareholders in the annual general meeting held on 9 June 2022 and paid to shareholders on the register at the close of business on 10 June 2022.

9. Principle Risks and Uncertainties

There are a number of potential risks and uncertainties which could have a material impact on the Group's performance over the remaining six months of the financial year and could cause actual results to differ materially from expected and historical results. The directors do not consider that these have changed since the publication of the annual report for the year ended 31 December 2021, which contains a detailed explanation of the risks relevant to the Group on page 26, and is available at www.sopheon.com. Other risks and uncertainties of the Group are disclosed in the Chairman’s Statement and the notes to the interim financial information included in this half-yearly financial report. In addition, the Board have continued to monitor and mitigate the effects of the following international events on the Group’s business:

COVID-19

The directors have continued to monitor and respond to the effects of the global COVID-19 pandemic on the Group. From the start, the board implemented an immediate work from home policy and travel restrictions, supported by well-defined virtual working practices, as well as assuring continuity of business operations and cloud services. This went smoothly, and the Group continues to operate mostly virtually today, with a blend of home and office working expected. Some rationalization of office space has already been undertaken as leases permit, and this is expected to continue.

Brexit

The effects of the UK’s withdrawal from the EU has not had a significant impact on the Group, due to the global geographical footprint of the business and the nature of its operations. However, the directors and management continue to monitor the situation to manage the risk of the return of volatility in the global financial markets and impact on global economic performance.

War in Ukraine

In February 2022, Russia invaded Ukraine leading to a strong sanction response by many jurisdictions around the world including by the UK, USA and EU. Sopheon is committed to honoring the sanctions imposed on Russia, named individuals, and business entities. In addition, Sopheon, like many companies worldwide, has suspended all business activity with Russian entities. Although Sopheon does not have any active customers in Ukraine or Russia, prior to the invasion the Group was involved in a small number of material sales opportunities within the territory, which have been suspended. This is not expected to have any impact on the Group's ability to continue as a going concern.

10. Cautionary Statement

This report contains certain forward-looking statements with respect to the financial condition, results of operations and businesses of Sopheon plc. These statements are made by the directors in good faith based on the information available to them up to the time of their approval of this report. However, such statements should be treated with caution as they involve risk and uncertainty because they relate to events and depend upon circumstances that will occur in the future. There are a number of factors that could cause actual results or developments to differ materially from those expressed or implied by these forward-looking statements. Nothing in this announcement should be construed as a profit forecast.

This announcement contains inside information as defined in article 7 of the market abuse regulation EU NO. 596/2014, as retained and applicable in the UK Pursuant to S3 of the European Union (withdrawal) ACT 2018 ("MAR").

Independent Review Report to Sopheon PLC

Conclusion

Based on our review, nothing has come to our attention that causes us to believe that the condensed set of financial statements in the half-yearly financial report for the six months ended 30 June 2022 is not prepared, in all material respects, in accordance with UK adopted International Accounting Standard 34 and the London Stock Exchange AIM Rules for Companies.

We have been engaged by the company to review the condensed set of financial statements in the half-yearly financial report for the six months ended 30 June 2022 which comprises the consolidated income statement, consolidated statement of comprehensive income, consolidation statement of financial position, consolidated cash flow statement, consolidated statement of changes in equity and associated notes.

Basis for conclusion

We conducted our review in accordance with International Standard on Review Engagements (UK) 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” (“ISRE (UK) 2410”). A review of interim financial information consists of making enquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other review procedures. A review is substantially less in scope than an audit conducted in accordance with International Standards on Auditing (UK) and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion.

As disclosed in note 2, the annual financial statements of the group are prepared in accordance with UK adopted international accounting standards. The condensed set of financial statements included in this half-yearly financial report has been prepared in accordance with UK adopted International Accounting Standard 34, Interim Financial Reporting.

Conclusions relating to going concern

Based on our review procedures, which are less extensive than those performed in an audit as described in the Basis for conclusion section of this report, nothing has come to our attention to suggest that the directors have inappropriately adopted the going concern basis of accounting or that the directors have identified material uncertainties relating to going concern that are not appropriately disclosed.

This conclusion is based on the review procedures performed in accordance with ISRE (UK) 2410, however future events or conditions may cause the group to cease to continue as a going concern.

Responsibilities of directors

The directors are responsible for preparing the half-yearly financial report in accordance with the London Stock Exchange AIM Rules for Companies which require that the half-yearly report be presented and prepared in a form consistent with that which will be adopted in the Company's annual accounts having regard to the accounting standards applicable to such annual accounts.

In preparing the half-yearly financial report, the directors are responsible for assessing the company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the company or to cease operations, or have no realistic alternative but to do so.

Auditor’s responsibilities for the review of the financial information

In reviewing the half-yearly report, we are responsible for expressing to the Company a conclusion on the condensed set of financial statement in the half-yearly financial report. Our conclusion, including our Conclusions Relating to Going Concern, are based on procedures that are less extensive than audit procedures, as described in the Basis for Conclusion paragraph of this report.

Use of our report

Our report has been prepared in accordance with the terms of our engagement to assist the Company in meeting the requirements of the rules of the London Stock Exchange AIM Rules for Companies for no other purpose. No person is entitled to rely on this report unless such a person is a person entitled to rely upon this report by virtue of and for the purpose of our terms of engagement or has been expressly authorised to do so by our prior written consent. As above, we do not accept responsibility for this report to any other person or for any other purpose and we hereby expressly disclaim any and all such liability.

BDO LLP

Chartered Accountants & Registered Auditors

Gatwick, UK

23 August 2022

BDO LLP is a limited liability partnership registered in England and Wales (with registered number OC305127).